When the 6 month grace period ended and the time came for me to start paying off my student loans, I bought 5 containers of Ben and Jerry’s. I’m not kidding. I actually sat in front of my computer, holding back tears in panic mode, inhaling ice cream.

If you’re like me, swimming in debt, this is something you have to confront pretty quickly, likely before you’re even close to being ready to. Student loans are ominous, stressful and confusing to most of us. Resources and education also feel incredibly lacking online. Basically, you have to pull together your own plan of attack. I’ve learned pretty quickly, through trial and error, some tips for wrangling nasty student loan debt. From budgeting to spreadsheets, hopefully I can drop some Ben and Jerry’s binge night student loan knowledge.

1. Do your research. Ask for help if you need it.

The first step to feeling more comfortable about paying your student loans is understanding them. Take the time to actually digest the federal loan training you have to do, and look at other resources for your private loans. SALT is a good option. They have a community board where you can directly ask questions, and there is information for students in a variety of loan situations. Student Loan Hero is another great resource. They provide helpful articles, calculators and various tools for managing student debt.

2. Understand your options for lower payments.

If you’re staring in the face of multiple loans, the ending balances can sometimes be unmanageable for your current income. There are options for lessening your monthly payments in the beginning when you’re not making as much money, and having those payments increase as time goes on. Federal loans offer a number of opportunities right there on the site. You just have to submit the request and await approval. Private loans make it a little more tricky. You’ll have to call your student loan provider and ask about your options, and at that point someone can help you. Don’t even try to find a way around calling. Calling is for some reason the only way to actually get this done, and having a conversation with a real person is actually super comforting.

I still urge you to be mindful of the decision to change payment plans. If you can fit the regular payments into your budget now with some cuts to disposable income, then do that. The less money you pay now, the more interest builds up and the more you pay later. The lower payments should only be used if they actually are unaffordable for you. Otherwise, you’re just deferring a portion of your payments that will occur more interest over time, making you pay way more in the end.

3. Create a system of tracking payments.

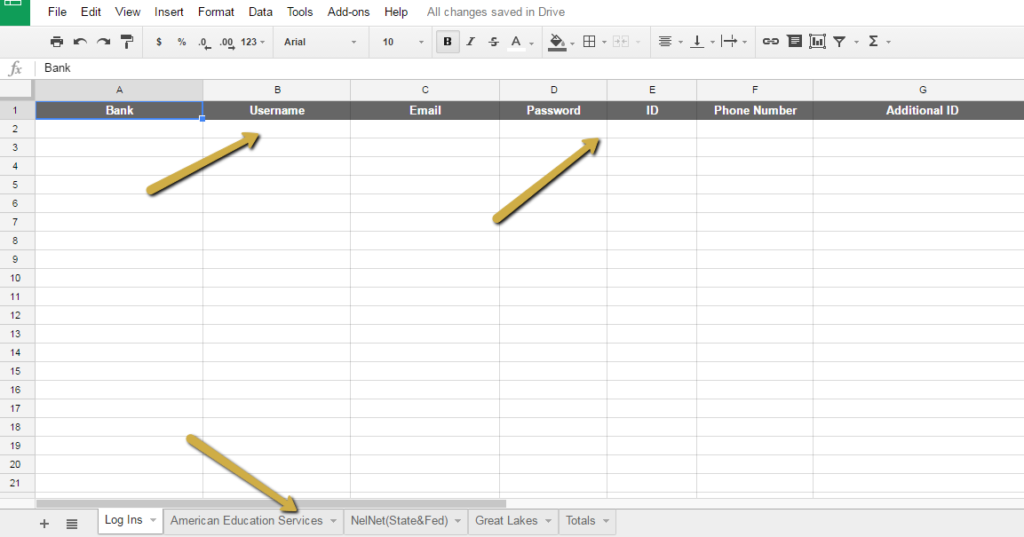

This is something I 100% recommend doing. Make a spreadsheet and track your loan information, payments, username credentials and everything you need to keep record of your payments. I recommend using Google Sheets on Google Drive, because it keeps the record safe through different computers and you can access it at any time.

Here is an example of the first sheet in the document, containing all username, password and ID information because wrangling all of that can be one of the hardest parts.

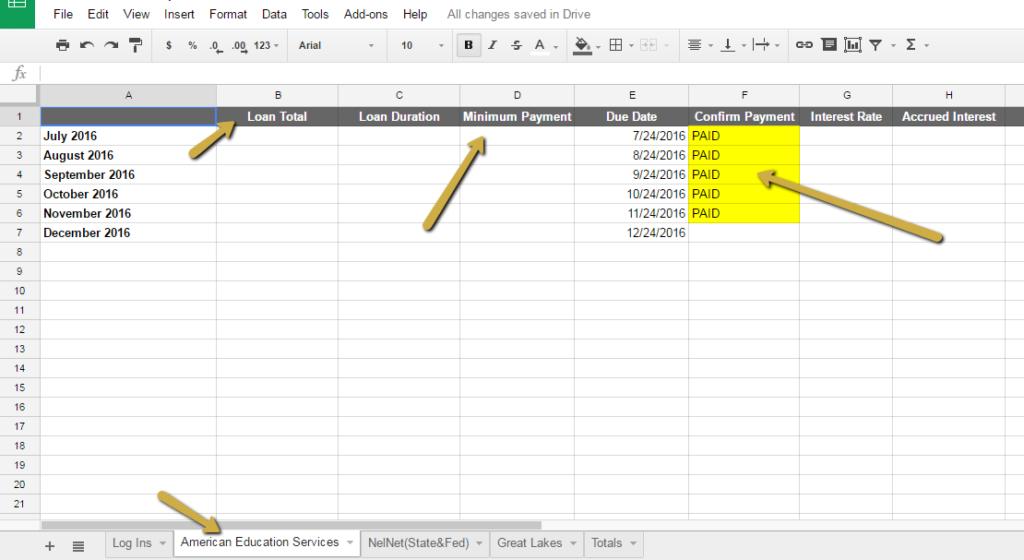

At the bottom is where each of the individual loans are listed and tracked within each sheet. This is an example of mine with the info cleared out, but you can make a copy of this document for every loan.

Here you can track minimum payments, due dates, loan progress and anything else you need to to wrap your head around each loan’s details.

4. Research loan consolidation and see if it’s right for you.

I’m going to break down consolidation into two parts, State/Federal and Private Loans, because that was the easiest way for me to understand it when I was learning.

My opinion: Your state and federal loans have lower interest rates than private loans. You wouldn’t want to consolidate all of those loans together, as it would likely raise your interest rates for the state and federal portion of your debt. Everyone is different, but I personally think State and Federal loans should live in their own little happy lower interest rate land, separate from privatized loans.

State and Federal Loan Consolidation: Every state and federal loan you received for every semester is logged as a separate loan. What?! This was me when I saw 14 different loans come up on my computer from only one freaking source:

But don’t worry, there’s an easy fix for this one. Here’s everything you need to know about consolidating your state and federal loans –> https://studentaid.ed.gov/sa/repay-loans/consolidation. It’s a different process than the full student loan refinancing I am going to talk about next, because it takes place exclusively within your state and federal loan provider. It took a week to process and I received notification in the mail that I was good to go, and those 14 loans became one.

Private Loan Consolidation: As mentioned above, some people consider this option for both state/federal and private, but for the purposes of describing this from my own perspective and opinion, I’m recommending it for private loans specifically.

Wait, what the heck is student loan consolidation and refinancing? Good question. Basically, one bank buys up your loans from a bunch of banks. Then you just have to pay that one bank instead of the 3 or 4 banks that previously owned each of your loans. Additionally, it can again help you obtain lower monthly payments if needed.

So, what’s the catch?

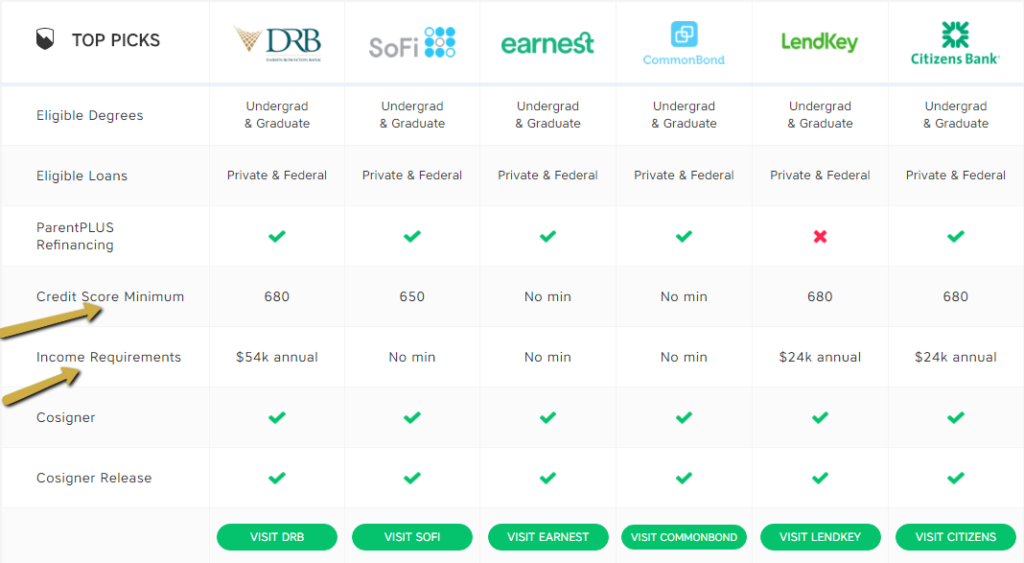

To start, you have to qualify for a good student loan consolidation. It can often require a co-signer, good credit and significant income if you’re actually going to get a better deal with the consolidation. Student Loan Hero breaks down examples of those qualifications for the different banks and providers pretty well in this graphic.

There are also some fees involved. You may have to pay an origination fee. This could be up to 2 percent of the total you refinance. So, say you have $70,000.00 in loans to refinance and the fee is in fact 2%, that’s $1,400.00 for that fee that you owe to your refinancing provider over time.

Also, not all Student Loan Consolidation providers are legitimate. If you find some site promising you benefits that seem too good to be true, trust me, they probably are too good to be true. Forbes wrote a great piece about the rise of Student Loan scams that you should check out before conducting individual research into providers.

Student Loan Hero lists a number of Pros and Cons to student loan consolidation here.

5. Manage your budget. Student loans are unfortunately here to stay, and they have to be a part of your plans.

This discussion of crushing student loans was virtually obsolete for other generations. The concept of drowning in $70,000.00 in debt when you’re 22 didn’t exist until recently, and like anything new, it’s terrifying. It’s terrifying, but it’s manageable. I promise. We just have to learn how to be financially conscious and educated very early on, and in a lot of ways that’s not necessarily a bad thing. I was 21 years old and had to learn how to manage more bills than any Home Ec teacher ever said existed. But that’s OK. Mortgages and other huge life expenses seem much less ominous now. Learning about your options as a young professional is really important, and so is having a plan.

You just have to be mindful of your budget. Everyone, and I mean EVERYONE, hates budgeting. But you need it if you’re going to manage debt responsibly. Mint is a great app to track your spending, and so is creating an old fashion spreadsheet to manage your larger monthly bills. Even if it’s a fairly rough estimate, you should know how much disposable income you actually have.

Failing to pay monthly payments is a slippery slope that can lead to defaulting on your loans, a devastated credit score and future financial setbacks that you absolutely want to avoid. The current student loan predicament in this country is blasphemous. But the right amount of determination, mindfulness and perseverance can overcome any challenge in this world, and trust me, this is no exception.

There you have it. Now, go forth and kick some student loan ass.

Have any questions or tips for paying back your student loans? Let us know in the comments below!